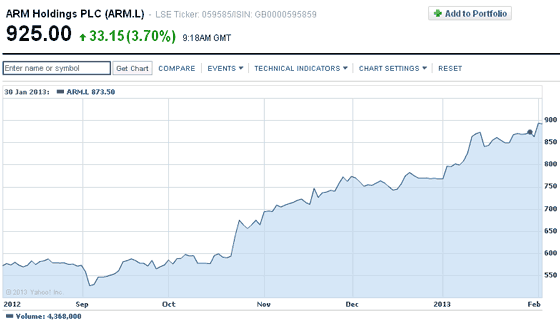

Cambridge based microchip designer ARM today released its financial results for Q4 2012. The headline figures are that the company made a pre-tax profit of £80 million on revenue of £164.2 million. The results soundly beat analyst expectations; the market consensus was that profits would be £75.6 million on £152.2 million pounds of revenue. As I write shares in ARM are up approximately five per cent at 935p. In the last 12 months the company’s share price has risen by over 60 per cent.

In a statement accompanying the results CEO Warren East said “Customers are developing products to meet the needs of the post PC era and are driving demand for ARM’s most advanced technology. 2013 brings exciting opportunities and challenges as ARM enters competitive new markets where we are well positioned to succeed.” Also, importantly, customers of ARM are paying higher royalties due to the popularity of the Cortex-A and Mali series of chips.

The growing popularity of using smartphones and tablets for trivial computing tasks, communications and entertainment is well documented upon HEXUS. Only a few days ago we brought you news about the soaring tablet market; tablet shipments are up 75 per cent from just a year ago. Likewise smartphones are on the up; the worldwide smartphone market grew 36 per cent in Q4 2012 with nearly 220 million units shipped, according to IDC’s latest figures. Despite all the popularity of these miniature computing devices we were also happy to report, just over a month ago, that analysts have decided tablets will not kill PCs!

Bloomberg reports that ARM started Q4 2012 with a record order backlog. I’m sure both AMD and Intel wouldn’t mind helping out a bit, but both these chip dinosaurs, known to be making concerted efforts in mobile chip design, aren’t matching ARM’s power/watt ratios as yet. Also their task isn’t just matching ARM, to beat an established company in any market you usually have to offer something significantly better; a compelling reason for buyers to jump ship.